Transfer Pricing for Commodity Entities, what type of trader is your company?

Home • Insights • Transfer Pricing for Commodity Entities, what type of trader is your company?

Home • Insights • Transfer Pricing for Commodity Entities, what type of trader is your company?

The Inland Revenue Authority of Singapore (IRAS) recognises the diversity in the commodity marketing/trading (CMT) activities undertaken by CMT entities in Singapore and the wide-ranging values they could bring to their multinational enterprise (MNE) group.

A CMT entity may act at different levels of the market across a range of customers, suppliers and commodities, or transact with the same party at different times or under different circumstances for various commercial objectives.

Depending on the MNE group arrangement, a related party commodity transaction can take many forms.

In this article, we will analyse how these businesses are being set up, the supply chain involved and the potential challenges in applying

transfer pricing methods to test the related party commodity transactions.

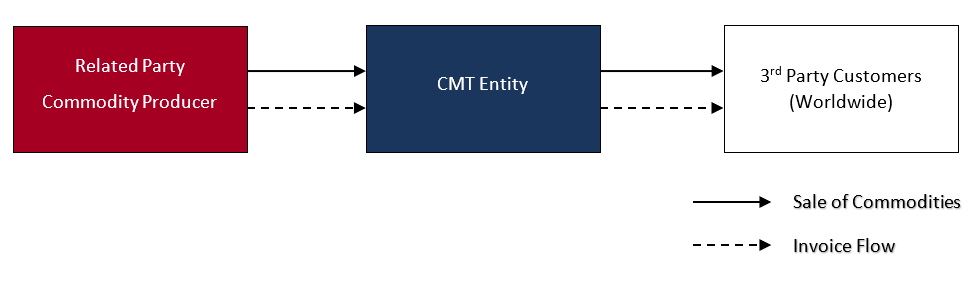

BUSINESS STRUCTURE

In addition to serving the local market, commodity producers may seek to expand its trading network by selling commodities to overseas customers. Instead of operating from their home country, commodity producers are likely to establish CMT entity in global commodity hubs due to the extensive network of buyers and sellers and sound financial and trading infrastructures (e.g. financial institution, processing and storage facilities, shipping companies).

The marketer/distributor could be responsible for:

POTENTIAL APPROACHES & CHALLENGES

Comparable Uncontrolled Price (CUP) Method may be appropriate by applying the quoted price CUP (e.g. Index Price publicly available) to test the commodity price. The biggest challenge with the CUP method is:

The three issues above need to be considered to decide on how the CUP method will be applied e.g. on samples, by shipment.

Resale Price Method: Marketer/distributor are commonly remunerated by reference to sales values by earning a percentage

discount (or gross margin) from the sale price. The Resale Price Method (RPM) can be applied by reference to either independent commission

rates (to determine gross margin) or the gross margin earned by internal/external comparables.

Transactional Net Margin Method (TNMM) – Operating Margin (OM) may also be appropriate to test the distribution activities.

Based on the transfer pricing guidelines on CMT activities released by IRAS

(E-Tax guide), commodity trading could involve other value-adding activities such as collecting real time market intelligence, managing

logistics, maintaining customer relationships. Therefore, this method may be unreliable if the marketer/distributor makes

valuable contributions to the related party commodity transaction.

Nonetheless, IRAS states that TNMM – OM may afford a practical solution to otherwise insoluble transfer pricing problems when used sensibly

with appropriate adjustments to comparable independent party transactions to account for differences.

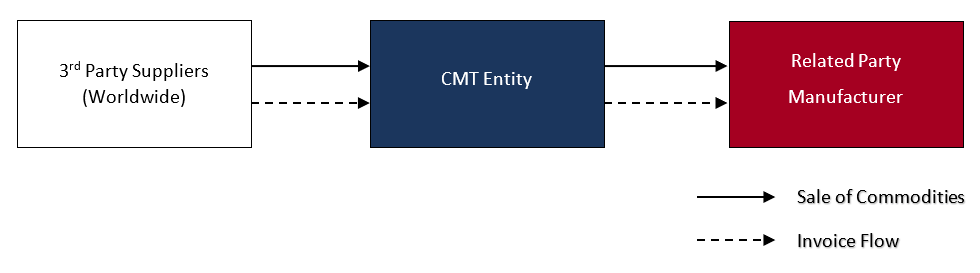

BUSINESS STRUCTURE

Commodities are commonly used as raw materials to manufacture finished goods. These commodities are required in large volumes by manufacturers. Therefore, MNE groups may seek to establish procurement entity in commodity hubs to ensure continuous supply of raw materials. In addition, the availability of a wide range of financial institutions, foreign exchange clearing houses and hedging solutions allows the procurement entity to source commodities in a cost-effective manner and reduce the MNE group’s exposure to various risks (e.g. adverse movement in commodity price).

The procurement entity could be responsible for:

POTENTIAL APPROACHES & CHALLENGES

Similarly, the quoted price CUP can be applied to test the related party commodity transaction but may prove difficult to use if the volume of transactions during the year is high. In addition, it may be difficult to identify comparable independent commodity transactions due to them being highly confidential and publicly unavailable.

The RPM may also be utilised by reference to either independent commission rates (to determine gross margin) or the gross margin earned by internal/external comparables. However, taxpayers should take into consideration the level of operating expenses incurred by the procurement entity such as finance costs, hedging costs and insurance associated with commodity purchases. Attention should be given to the procurement entity’s remuneration to determine if it is sufficient to cover these operating expenses and earn an arm’s length profit.

We found frequent mistakes on traders that monitor the gross margins and do not track whether their margin is sufficient to cover their operating expenses leaving an arm’s length net profit for the procurement trader entity.

TNMM – OM can be more appropriate if the trader wants to test whether its gross margin is sufficient to leave an arm’s length profitability

for the procurement entity.

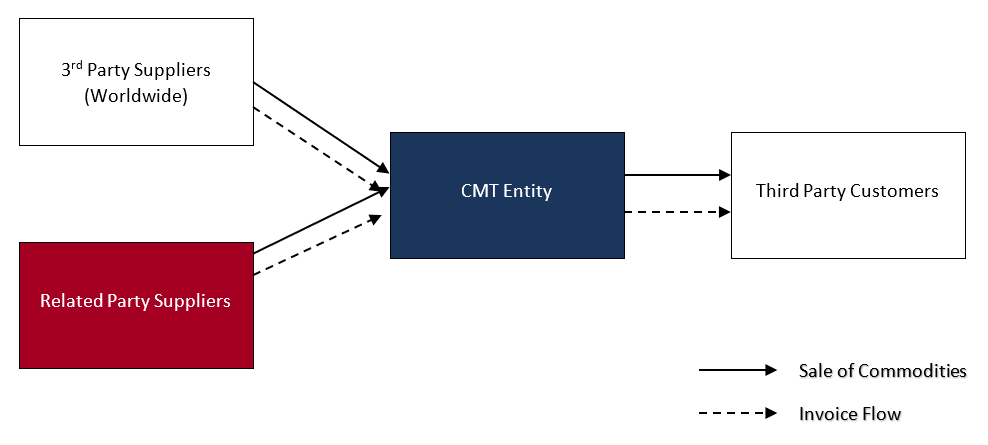

BUSINESS STRUCTURE

Based on the e-Tax guide, a CMT entity may operate as a full risk-taking entrepreneur – purchasing commodity from multiple sources (i.e. from the MNE group and/or third parties) and be fully responsible for trading and maintaining market for the commodity on its own account. The commercial objectives for operating as a full-fledged trader include balancing the market, aligning diverse suppliers and customers, taking on commitment to allow project investments, acting as central management for shipping, storage and risk management through physical and derivative transactions.

Key trading executives with specialized expertise on logistics, financing, hedging and trading would be stationed in such CMT entity to

perform these functions.

POTENTIAL APPROACHES & CHALLENGES

A full-fledged trader may trade in multiple commodities from multiple suppliers (related party and third party) around the world. While internal comparable transactions may have a more direct and closer relationship to the transaction under review, it may be difficult to apply the Internal CUP to test the entire related party commodity transaction due to various factors such as different commodity type and quality, shipping terms, pricing formula and pricing date. Hence, it may be more practical and reliable to use quoted price CUP in such situations.

As explained earlier, the e-Tax guide has stated that TNMM – OM is unlikely to be an appropriate method to price valuable contributions and risk-taking entrepreneurial activities in relation to commodity trading Alternatively, taxpayers may consider applying internal TNMM by comparing the OM of related party segment and third party segment if both segments are functionally comparable.

Segmentation of the full-fledged trader’s financial results can be performed in the following steps:

QUESTIONS

Australia | +61 (3) 59117001 | reception@transferpricingsolutions.com.au

Singapore | +65 31585806 | services@transferpricingsolutions.asia

Malaysia | +603 2298 7153 | services@transferpricingsolutions.my

Contributed by TPS consultant Samuel Tay

Samuel was attached to two international accounting firms prior to joining Transfer Pricing Solutions Asia. He has prepared transfer pricing documentation for clients from the Asia Pacific region (e.g. Malaysia, Singapore and Australia).

His expertise includes handling transfer pricing engagements and conducting benchmarking studies for companies from various industries such as oil and gas, shipping, chemical, wood, jewellery and the electronics industry.

In his spare time, Samuel enjoys reading and playing sports.

Contributed by TPS Director Adriana Calderon

Adriana is the co-founder of Transfer Pricing Solutions Asia and Transfer Pricing Solutions Malaysia and Lead Partner in Asia.

Adriana has extensive international experience with Big Four and mid-tier firms advising multinational companies in the areas of corporate

and international taxation across South America, the US, Australia and the Asia Pacific Region.

As a TP practitioner, Adriana has advised companies in the Asia Pacific Region across various industries and in a wide range of projects associated with planning.

Adriana also enjoys teaching and is a regular speaker and facilitator of Transfer Pricing seminars and workshops in Singapore. She is a

transfer pricing trainer for the Institute of Singapore Chartered Accountants and Singapore Institute of Accredited Tax Professionals.

Adriana lives in Singapore with her family and is a mother to two energetic boys.