Iras Updates Indicative Margins For Related Party Loan

Home • Insights • Iras Updates Indicative Margins For Related Party Loan

Home • Insights • Iras Updates Indicative Margins For Related Party Loan

.jpg)

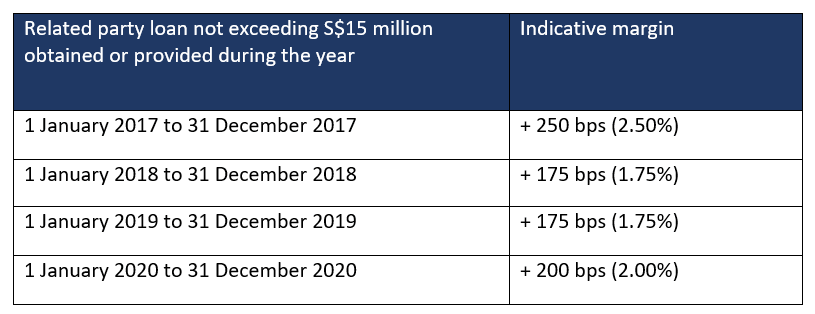

Inland Revenue Authority of Singapore (“IRAS”) has introduced the indicative margins for related party loans since the past few years whereby the indicative margins are updated at the beginning of each calendar year. The indicative margins are applied on each related party loan not exceeding S$15 million.

The indicative margins introduced by the IRAS for each of the years are provided in the table below:

If taxpayers choose to apply the indicative margin, they will apply the indicative margin on the appropriate base reference rate selected for the related party loan. For example:

Examples of base reference rates for floating rate loans are:

Examples of base reference rates for fixed rate loans are:

The indicative margin is not mandatory. It gives taxpayers an alternative to performing detailed transfer pricing analysis in order to comply with the arm’s length principle for their related party loans.

If taxpayers choose not to apply the indicative margin or if it is not applicable to them, they will have to apply an interest rate in line with the arm’s length principle and maintain contemporaneous transfer pricing documentation.

Details of the 3-step approach to determine the arm's length interest charges for related party loans and guidance on applying the administrative practice for indicative margins on related party loans is provided in Part III, Section 13 of the Transfer Pricing Guidelines.

Contributed by TPS Director Adriana Calderon

Adriana is the co-founder of Transfer Pricing Solutions Asia and Transfer Pricing Solutions Malaysia and Lead Partner in Asia.

Adriana has extensive international experience with Big Four and mid-tier firms advising multinational companies in the areas of corporate

and international taxation across South America, the US, Australia and the Asia Pacific Region.

As a TP practitioner, Adriana has advised companies in the Asia Pacific Region across various industries and in a wide range of projects associated with planning.

Adriana also enjoys teaching and is a regular speaker and facilitator of Transfer Pricing seminars and workshops in Singapore. She is a

transfer pricing trainer for the Institute of Singapore Chartered Accountants and Singapore Institute of Accredited Tax Professionals.

Adriana lives in Singapore with her family and is a mother to two energetic boys

Questions?

Contact Transfer Pricing Solutions. We can assist with the preparation of transfer pricing documentation locally and regionally, Master File and Local File to comply with the OECD and also local legislation.

Australia

+61 (3) 59117001

reception@transferpricingsolutions.com.au

Singapore

+65 31585806

services@transferpricingsolutions.asia

Malaysia

+ 603 2298 7153

services@transferpricingsolutions.my