All you need to know about Indonesia New Transfer Pricing Rules

Home • Insights • All you need to know about Indonesia New Transfer Pricing Rules

Home • Insights • All you need to know about Indonesia New Transfer Pricing Rules

The Indonesian transfer pricing landscape continues in turmoil, where Companies are struggling to understand and comply with the latest released regulation No. 213/PMK.03/2016 (“PMK-213”).

PMK-213 introduced BEPS Action Plan 13 in Indonesia implementing the three-tiered transfer pricing documentation approach, i.e., Master File, Local File, and Country by Country Report (“CbC Report”). PMK-213 is effective from 30 December 2016; its purpose is to strengthen the quality of transfer pricing document while promoting transparency in between tax jurisdictions.

Yes, as long as you have related party transactions, you will need to prepare documents. Taxpayers with transactions between Indonesia and countries with lower tax jurisdiction (like Singapore) are particularly impacted as they will have to prepare documentation regardless of the total gross revenue and the total value of the related party transaction.

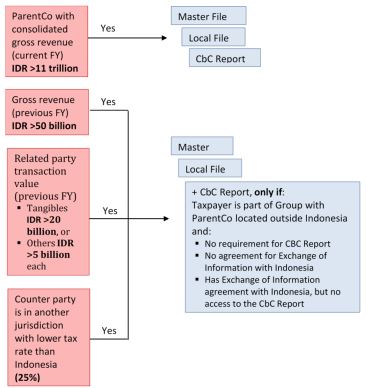

The level of documentation needed depends on whether you meet the following criteria.

If you’re saying no to all of the condition above, your company does not need to prepare a transfer pricing documentation, but still needs to apply the arm’s length principle when dealing with related parties.

The Master File should at least include:

The Local File should at least include:

If your company is involved in more than one business activity, then the information above should be presented separately (segmented).

The CbC Report should at least include:

Working papers for the preparation of the CbC Report are to be attached during submission.

The deadline for transfer pricing documentation is tight!

Master File and Local File must be ready within four months after the end of company’s fiscal year. CbC Report must be prepared and ready within 12 months after the end of company’s fiscal year.

Questions?

Contact Transfer Pricing Solutions

Australia

+61 (3) 59117001

reception@transferpricingsolutions.com.au

Singapore

+65 31585806

services@transferpricingsolutions.asia